development will be important in ensuring continued productivity gains of the magnitude required to limit local food security concerns.

It is estimated that in Asia and Oceania, there are around 12 million ha under certified organic production. Most of this land area is in Australia, with only a fraction of organic agriculture production attributable to Asia (Willer and Yusefi, 2005). Organic agriculture is of increasing interest to both NGOs and agribusinesses because it offers a new sustainable development business opportunity. In addition, organic agriculture is considered to offer potentially higher incomes due to lower energy requirements, decreased water and pesticide inputs, and because it buffers yields against drought (Pimental et al., 2005).

4.2.2.3 Commodity prices

Theoretically it is expected that over time the prices of primary food commodities will decline relative to prices of manufactures as a result of (1) wage and productivity differentials between low income countries that typically produce primary commodities and higher income countries that typically produce manufactures, and (2) lower income elasticity of demand for primary commodities (Prebisch, 1950; Singer, 1950). This globally worsening terms of trade portends progressive squeezing of the rural economies in ESAP where a majority of the population still subsists on agriculture.

History reveals a downward trend in the prices of agricultural commodities as productivity in the agricultural sector and technological advances have been made, with some fluctuations caused by weather conditions. Particularly prior to the current resurgence of globalization since the 1990s, most developing countries kept their domestic food prices below global food prices and artificially raised the price of manufactured goods above international prices. Gradual changes and reductions in tariffs, as well as new |

|

import and export regimes have changed these price regimes in the ESAP region.

Commodity and energy prices are interlinked. High energy prices translate into higher commodity prices vis à vis manufactures. For example, the highly energy intensive production of fertilizers can affect the prices of agricultural products by raising input costs (ADB, 2006b). High oil prices may also result in increased demand for biofuels as consumers substitute least cost fuel sources. This may have implications for local food security in some regions (see 4.9.1) if demand for biofuels is strong enough to displace traditional agricultural food crop production.

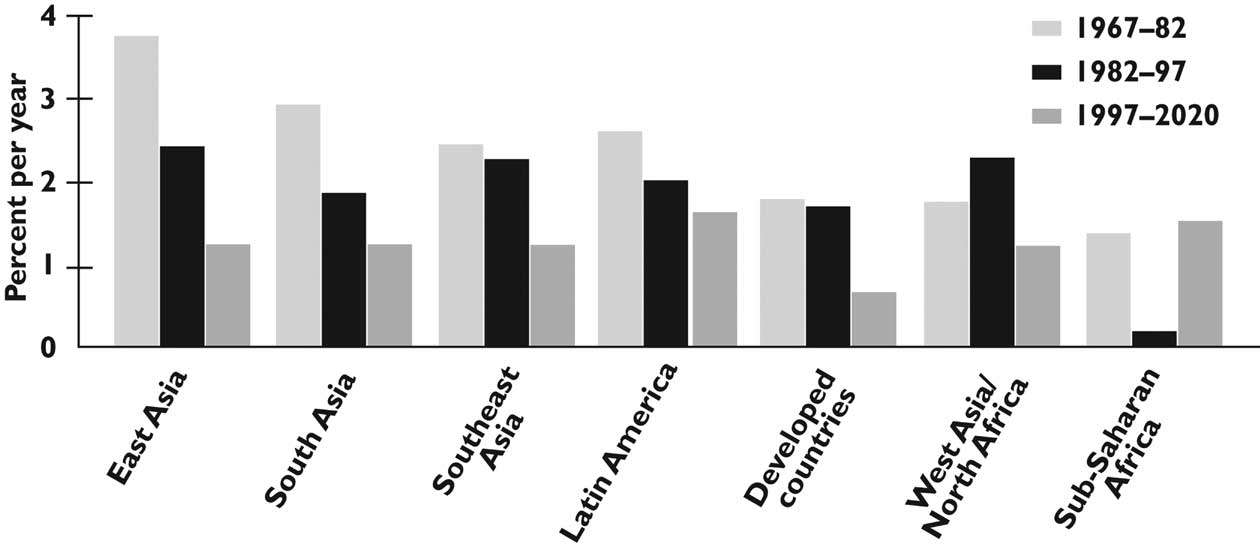

Projected real agricultural commodity prices are expected to fall by 2015, relative to 2001 levels. ADB (Park and Zhai, 2006) presents a range of commodity price projections to 2015 under three scenarios. The scenarios centre around a baseline, with assumptions about higher and lower agricultural TFP growth, energy efficiency and energy reserves. The disaggregated impacts of the softening and tightening variables are given alongside the aggregate impacts on commodity prices. Changes in agricultural productivity are associated with roughly equivalent percentage changes in world agricultural commodity prices. Energy security and environmental constraints represent two significant uncertainties that could affect projections of agricultural commodities prices into the future (see 4.2.7, 4.2.8 and 4.2.9).

4.2.2.4 Globalization, economic growth and agricultural markets

Industrialization in agriculture has resulted in the coordination, production and distribution of produce to a larger market. Improvements in transport and information networks have a tendency to increase mobility between suppliers around the world. The higher degree of access to a variety of goods has assisted in integration along the supply chain including between abattoirs, supermarkets and other |